In New SEC Filing, Company Reveals Onkyo, Rosen, and VSM No Longer Have Any Goodwill

Voxx International Corporation (Nasdaq: VOXX) has released its Form 10-Q report to the Securities and Exchange Commission (SEC) revealing its financial results for its third quarter – the 90-day period ending on November 30, 2024 – as well as the year-to-date nine-month period ended the same date for Fiscal 2025. It is a sobering report of a company struggling to get to the altar with Gentex while its financial foundation is increasingly shaking.

The surprising results answer some questions, yet raise others as revenues continue to decline and losses mount.

Learn more about Voxx’s current financial situation…

When we last heard from Voxx, the company was late in producing its routine quarterly earnings report and filed a Form 12b-25 with the SEC, saying its “triggering events review” was forcing it to engage in an interim detailed analysis to “test its goodwill, other intangible assets and other long-lived assets for impairment.” Not only that, but the Nasdaq Stock Market discovered this missed report and sent Voxx a warning letter that it was out of compliance with its listing rules and would need to cure this situation or face possible delisting from the exchange.

The Company Never Revealed Why It Needed to Test Its Value or What Triggered That Review

The timing for this interim impairment review was extraordinary and the company never said specifically what triggered it. The purpose of a formal interim impairment analysis is to review whether the value of its assets as carried on the company’s books is reasonably accurate. This is always important and companies regularly conduct such events at least annually…but for Voxx it is doubly important at this extraordinary moment in time as the company is in the midst of serious due diligence in connection with an agreement to be acquired by Gentex Corporation.

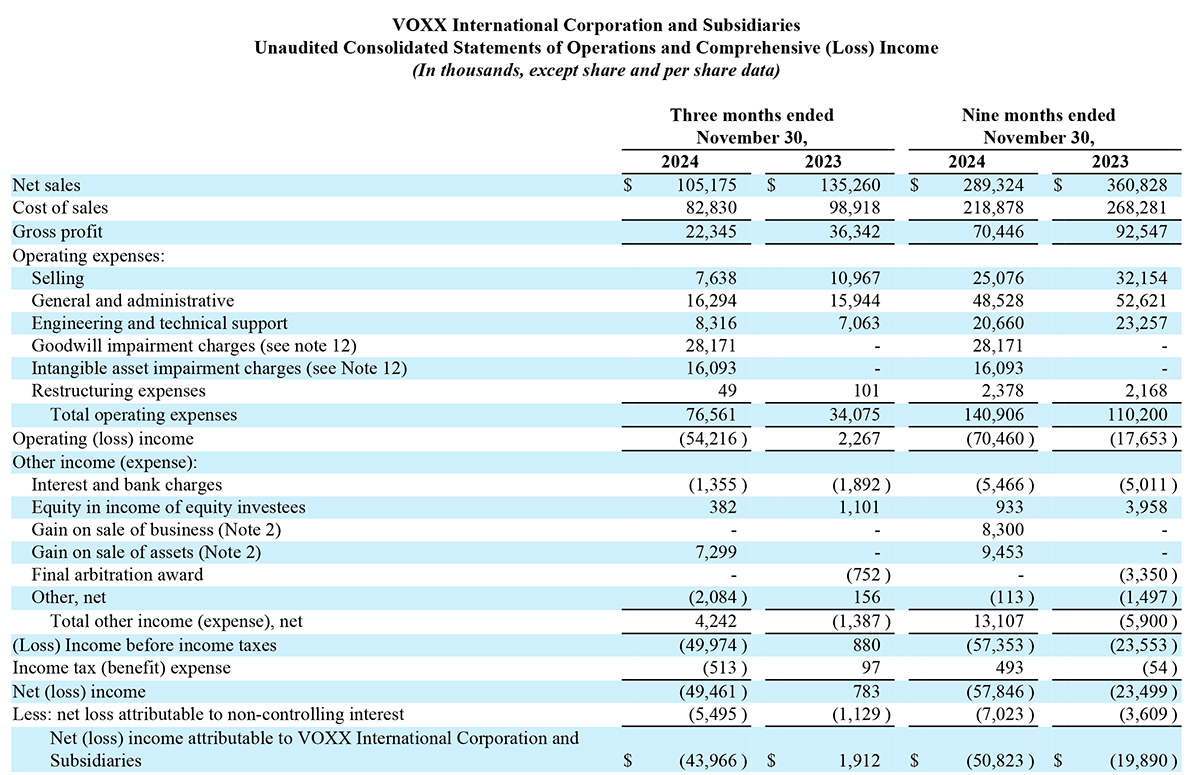

Now Voxx has finally filed its official 10-Q quarterly financial results and we learn in this new SEC filing that the company has concluded its interim review and as a result, has taken significant charges against earnings – and a charge to assets on its balance sheet – to write down the value of its carried goodwill, other intangible assets, and other long-lived assets…all components of the value of the brands the company has acquired over the years. It has taken these charges as those assets are significantly impaired. I will get into the details of all of that, but first, let’s dig into some of the key performance data for Voxx in its latest quarter and first three quarters (year-to-date or YTD) of Fiscal 2025.

Total Net Sales Drop Another 22.2% in 3Q of Fiscal 2025

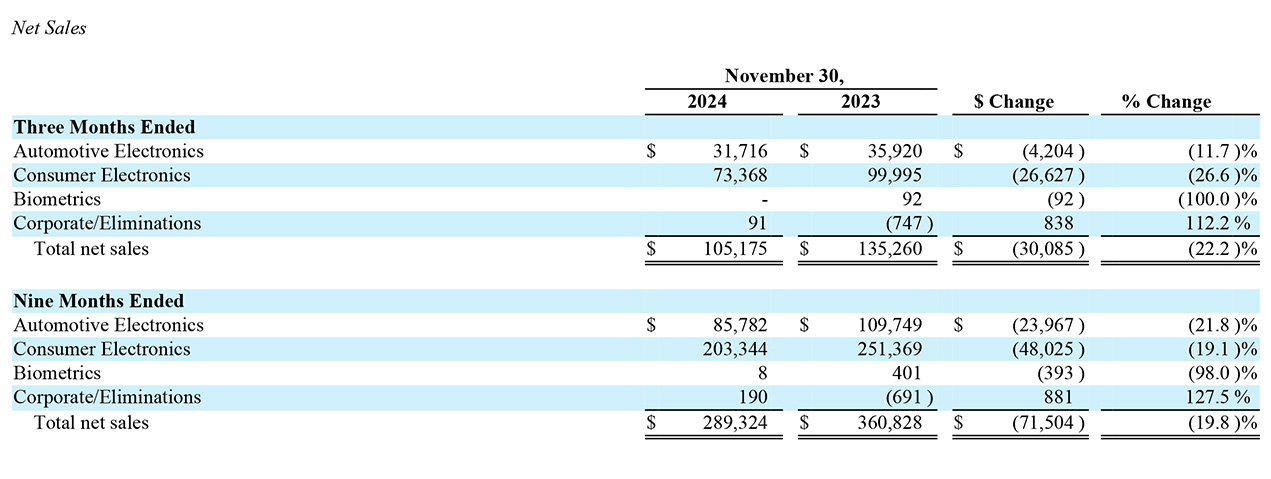

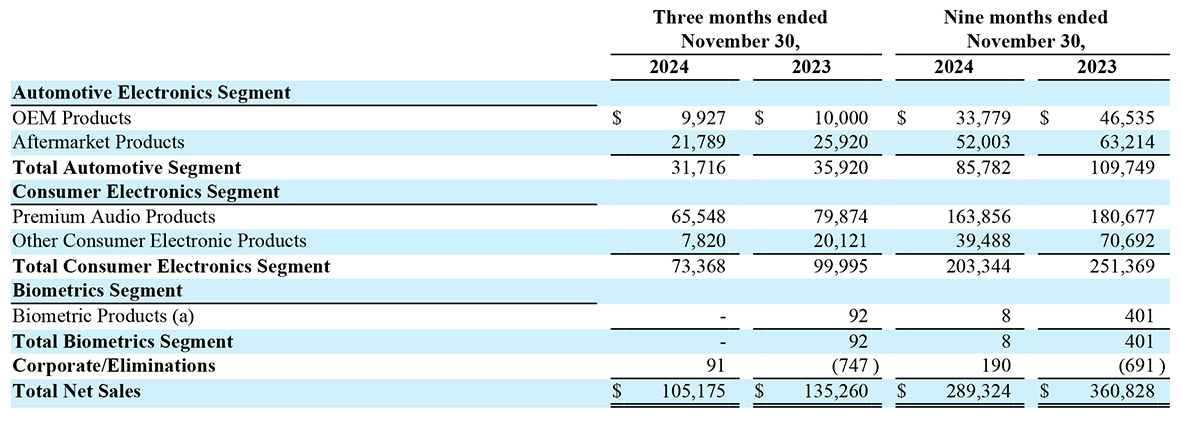

As long-time readers of Strata-gee know well, Voxx has three main business units: Automotive Electronics, Consumer Electronics, and Biometrics. The Consumer Electronics unit is most interesting to me, as this is the division that owns the Onkyo, Integra, and Klipsch audio brands through Voxx’s Premium Audio Company (PAC) subsidiary and trades specifically in the consumer audio business.

In this third quarter report, we learn that total net sales came in at just $105.2 million, down $30.1 million or 22.2% as compared with net sales of $135.3 million in the same quarter the previous year. The company said this decline was due to “economic, retail and OEM manufacturing conditions, along with asset sales during Fiscal 2025.”

Asset Sales: The Blessing of Immediate Cash…The Curse of Lost Future Sales

The asset sales Voxx is referring to include its divestment of Voxx Accessory Corporation, as well as Jamo & Energy loudspeakers. The sale of these brands brought in tens of millions of dollars collectively and was largely used to pay down the company’s too-high debt.

But the reality is that this has shrunk down the size of the business and makes future sales comparisons pretty useless. However, I doubt that this is the only reason for their reported sales declines. I recently reported a formerly major customer of its PAC division, ProSource had dropped the PAC brands – including Onkyo, Integra, and Klipsch – from its assortment. This loss had to have a major impact on its outlook for the future.

YTD Net Sales Drop $71.5 Million to $289.3 Million; Gross Margin Drops a Stunning 5.7% to 21.2%

Net sales for the nine-month period came in at $289.3 million, down $71.5 million or 19.8% compared with net sales of $360.8 million in the same period in fiscal 2024. The company noted that all business units saw sales declines.

During the quarter this year, gross margins came in at 21.2%, down a distressing 570 basis points (5.7%) from the gross margin of 26.9% in the same quarter the previous year. The company notes that the main reason for this dramatic decline in gross margins is due to inventory write-downs both in the Automotive Electronics and Consumer Electronics segments

The 800-Pound Gorilla Stomping on Voxx Results – The Company and Its Brands Have Less Value

This seems to be the best time to pause my review of the Voxx results to talk about the key issue that forced the company to reassess its value. Let’s review a bit of recent history. Back in January, I reported that Voxx had unexpectedly notified the SEC that it was unable to file its normal quarterly earnings forms as is required of public companies.

The reason they were unable to make this required filing, they told the SEC, is, “…the Company has determined that it is necessary to test its goodwill, other intangible assets, and other long-lived assets for impairment.” This excuse immediately caught my eye for two reasons: 1) Federal regulators don’t like it when you don’t do what you are required to do, and most public companies make sure filings are always on time…and 2) The company had already agreed to be acquired by Gentex Corp AND the price (its “value”) was already set at $7.50 per share.

What the Heck is Going On?

What the heck is going on? At the time, it was not completely clear why the company suddenly decided that it needed to take another look at its value. But I now believe the clue to the answer of why the company felt this added step was necessary, was my recent report on ProSource dropping all of the Premium Audio Company brands. This major dealer buying group was rumored to be one of, if not the, largest customer of PAC – at least at one time in their partnership. With around 550 dealers as ProSource members, it is not easy to replace that amount of lost volume.

In Voxx’s 10-Q filing, it does not come out and say that directly, but they do offer a couple of intriguing tidbits. But first, I need to explain a little bit about the two major types of assets that companies have, and that acquirers get when they buy a company. The first of these is “tangible” assets which are physical things, such as buildings, machinery, inventory, and the like. The second is “intangible” assets which are not physical things, but assets that can add value to a company. An example of an intangible asset is a brand name…not a physical thing, but can have tremendous value in well-run companies.

Intangible Assets Exert Tremendous Influence on the Value of Assets and Companies

Intangible assets are accounted for in three classifications: goodwill, definite-lived intangibles (Voxx calls this classification “indefinite”-lived intangible), and long-lived intangibles. I don’t want to get too bogged down in these definitions, however, if this concept is confusing consider this example. You are a car enthusiast interested in adding to your collection of classic vehicles. Your buddy tells you he has a “cherry” 1957 Ferrari 500 TRC Spider. What is the price of this 67-year-old vehicle? Because it is a collector vehicle in excellent condition you’re going to pay probably around $10 million or more for it. That is, of course, WAY more than the cost of the metal parts, but that collector-passion factor – an intangible asset – causes it to be worth far more than the sum of its steel and bolts.

Value changes over time, either increasing or decreasing. But when you are a company and the value of the assets you own decreases below the value you have them at on your books – artificially inflating the value of your company – you must write them down.

And this is the difficult situation in which Voxx found itself entangled.

Voxx Reports a ‘Recent Worsening of Business Performance and Industry Outlook’

From the Voxx 10-Q: “In the third quarter, we reduced the near-term and long-term outlook of our Onkyo, Klipsch, Rosen, and VSM reporting units; our indefinite-lived trademarks; and certain of our long-lived assets based on recent worsening of business performance and industry outlook in both the consumer electronics and automotive electronics markets.” [Emphasis added] [Ed Note: VSM is Voxx Safety Manufacturing in its Automotive Electronics Segment]

This is most likely the “triggering event” that caused the company to take an “interim” look at its intangible asset valuation – something it normally does once a year except in the case of a triggering event, which then forces one on an interim basis.

Voxx Discovered ‘The…Market Value of the Total Company…Was Below…Book Value’

More from the Voxx 10-Q: “Additionally, the implied market value of the total Company, as indicated by the Agreement and Plan of Merger with Gentex on December 17, 2024…was below our recorded book value as of November 30, 2024.” [Emphasis added] This is a big Oh-Oh…you’ve discovered your company is not worth what you are telling people it is worth!

The company goes on to additionally reveal that – given the vicissitudes of the stock market – this situation (the stock price hits a value that is lower than the implied market value of the total Company) has happened before, but in those instances, it was viewed as a temporary decline and its stock value was “trending upward.”

Now…the Situation has Changed, Voxx’s Stock Decline is No Longer Temporary

Now, however, as the 10-Q filing notes, the situation has changed: “After the announcement of the Agreement and Plan of Merger, our stock price has stagnated and it is believed that the decline is no longer temporary. We viewed these events as potential triggering events…” and launched a new impairment analysis. [Emphasis added]

The impact of this situation is pretty significant. The company has determined that one element of its intangible asset – its goodwill – is impaired to the tune of $28.2 million, broken down as Onkyo ($14 million), Klipsch ($12.7 million), Rosen ($880K), and VSM ($572K). A total of $26.7 million was charged to the Consumer Electronics segment, while another $1.5 million was charged to the Automotive Electronics segment.

But these charges were just the beginning of further charges and write-downs.

From the Filing: ‘Onkyo, Rosen, and VSM…No Longer Ha[ve] Any Goodwill’

“These impairments were the result of reductions in projected cash flows due to lower projected sales volumes and profitability. As a result of these impairments the Company no longer has any goodwill attributable to the Onkyo, Rosen and VSM reporting units,” the company’s filing noted.

To put a finer point on it, the filing notes that the company performed both a qualitative and quantitative analysis. “The qualitative assessments considered significant declines in forecasted revenue and profitability due to the downturn in demand.” [Emphasis added]

Keep in mind that the Voxx impairment test was conducted on three key elements of intangible assets – goodwill, indefinite-lived assets (sometimes referred to as other intangible assets), and long-lived assets.

One Unnamed CE Brand Causes Another $1.3 Million Charge; $14.8 Million Charge Against ‘Long-Lived Assets’

Voxx also reported in its filing that “[t]he fair value of one indefinite-lived asset in the Consumer Electronics segment was less than its carrying value and accordingly, a non-cash impairment charge of $1.3 million was recorded for the three and nine months ended November 30, 2024.” It did not identify which CE brand this additional charge is attributed to, but I wouldn’t be surprised if it too was Onkyo (or Integra) as the company went on to say no further charges were necessary against the Klipsch brand.

Finally, the company reported that its test of the third category of intangible assets – long-lived assets – revealed the need for yet another impairment charge of $14.8 million. This total amount was broken down at $7.4 million in the Consumer Electronics segment and $7.4 million in the Automotive Electronics segment for the same three and nine month periods.

Different Accounting for Different Forms of Intangible Assets

How these impairment charges are accounted for varies by type of intangible asset – some are charged directly against profits as an added expense on the company’s Consolidated Statements of Operation, while others are applied on the Balance Sheet as a reduction in asset value. No matter how it is accounted for, all of these charges serve to reduce the total enterprise value of Voxx.

Finally – and then we’ll return to our regularly scheduled program – Voxx had this warning for investors: “The remaining goodwill at our Klipsch and DEI reporting units, our indefinite-lived asset, and other long-lived assets are at risk for future impairment as they do not have significant fair value above their carrying value.” [Emphasis added] Yikes!

Total Operating Expenses

Getting back to our analysis of Voxx’s performance in the third quarter and YTD of Fiscal 2025 – we find that Total operating expenses for the quarter came in at an eye-popping $76.6 million, fully $42.5 million or 124.7% higher than operating expenses of $34.1 million in the third quarter of fiscal 2024. And the reason for this extraordinary increase in total operating expenses is the primary subject of this report – the company was forced to write down the value of its brands by a stunning $44.3 million after it completed its interim impairment analysis, as discussed above.

This impairment charge included $28.2 million “goodwill impairment charges” and $16.1 million “intangible asset impairment charges.” Minus these charges, the company said that Total operating expenses would have come in at $32.3 million, down $1.8 million or 5.2% compared to the previous year’s third quarter.

Voxx Reports a Significant $44 Million Net Loss for the Quarter

The extraordinary impairment charges combined to hand the company a significant Net loss for the quarter of $44 million “attributable to VOXX International Corporation” versus a Net income of $1.9 million in the third quarter of last year. In fact, the total Net loss was just under $50 million, of which $5.5 million is “attributable to non-controlling interest.”

Assuming the company’s business stabilizes, this large $44 million net loss should be the end of it. But, as the company warned, remaining goodwill, indefinite-lived asset, and other long-lived assets remain at risk of future impairment, given that they do not have significant fair value above their carrying value. This means it would not take much of an operational blip to force another round of future impairment charges.

Financial Results on a Year-to-Date Basis

Basically, the pattern of results that hit this third quarter report is pretty much reflected in the nine month year-to-date results as well. In a nutshell, they are as follows…

- Total net sales of $289.3 million, down $71.5 million or 19.8% compared to total net sales of $360.8 million in the same period in fiscal 2024. Declines were in both the Consumer Electronics and Automotive Electronics segments.

- Gross margin of 24.3%, down 130 basis points (1.3%) as compared to gross margin of 25.6% in the same period last year. Gross margins were impacted by inventory write-downs in the third quarter.

- Total operating expenses of $140.9 million, a $30.7 million or 27.9% uptick as compared to total operating expenses of $110.2 million in the same nine-month period in the last fiscal year.

- Net loss of $50.8 million attributable to Voxx International Corporation versus a net loss of $19.9 million in the same period last year.

The company also noted a significant improvement to its balance sheet with total debt of $18.8 million as of November 30, 2024. This is down $54.5 million or 74.4% from the total debt of $73.3 million as of February 29, 2024. As I’ve mentioned above, the company has sold off several of its brands including Voxx Accessory Corporation, Jamo, and Energy loudspeakers and used the proceeds to retire significant amounts of debt.

No Financial Analyst Conference Call This Time; Progress with Regulators

Voxx announced that due to it being in the middle of a proposed merger transaction with Gentex Corporation, it will not be holding its usual quarterly earnings conference call with financial analysts.

The company also announced that it has made significant progress in terms of obtaining regulatory approval for this merger. A waiting period, as mandated by the Hart-Scott-Rodino Antitrust Improvements Act of 1976, has expired as of 11:59 p.m. Eastern Time on February 3, 2025. It has also said that the German Federal Cartel Office sent them a letter on January 27, 2025, that said that the proposed merger “does not meet the prohibition conditions under the German Competition Act, and the merger may be implemented.”

Barring any future litigation filed by any other relevant governmental authority, it would appear that the regulatory hurdle may have been satisfied.

What Does Gentex Feel About the Reduced Value of Voxx?

So with a $28.2 million “Goodwill impairment charge” and a $16.1 million “Intangible asset impairment charges” (total of $44.3 million) hit to earnings (in Operating expenses) and a $28.5 million “Goodwill” reduction and a $30.3 million “Intangible assets, net” reduction (total of $58.8 million) in asset reductions on the Balance Sheet, what will the impact of all of this be on the Gentex acquisition of Voxx? There is no way to know for sure, but one helpful thing to keep in mind is that the CEO of Gentex, Steve Downing, is on the Voxx Board of Directors. And while the Voxx board created a special committee to negotiate on Voxx’s behalf with Gentex (Downing can’t represent both sides of this transaction), as a board member, he likely was already aware of this information before it was made public.

Many merger agreements provide an escape hatch for performance shortfalls, but I can’t say if the Gentex/Voxx agreement has one. But it’s possible in the grand scheme of things that this drop in valuation will not be big enough to scare Gentex away. They might be able to seek to renegotiate the purchase price or let the transaction stand as is.

What Does Gentex Think?

As far as I can tell, Gentex’s interest in Voxx is more strategic and based on adjustments they believe they can make in managing the Voxx business that it believes will succeed in driving it into a more successful future. Gentex’s interest appears to be based less on Voxx’s current success.

Voxx is a $469 million business (in Fiscal 2024), and even though it appears that it will come in short of that number in Fiscal 2025, it still is a fairly robust…if challenged…business. Gentex is a $2.3 billion business which makes the Voxx acquisition easily digestible, but we’ll have to see how it sits in its stomach post-acquisition. And it is a business that Gentex apparently has plans for, although they have never really articulated what those plans are for investors yet.

So…we’ll just have to tighten our seatbelts and see where this vehicle takes us. But what a bumpy ride it has already been!

To learn more about Voxx International Corporation visit voxxintl.com.

See more on Gentex Corporation at gentex.com.

As usual, your analysis is so clear and thorough.. Impressive how you read through the lines of a 10Q report to gives us a glimpse on what’s behind the scenes.. Thanks a ton Ted for your work!

Between Voxx/Gentex and Masimo/Sound United, we’re certainly up for an interesting coming few years for HomeTheater market.. Is it me or it’s groundhog day? i.e. a B2B company that suddenly will wake up to a completely different reality and technical requirements.. I just fail to see the connection besides the automotive supplier element in this new couple.. Harman group is a completely different beast and been in the auto industry for a very long time.. Gentex has lots of cash but zero audio experience based from a quick look at their IP. Very different requirements than Hometheater/CE where these 3 amazing brand excel.. Even if today Onkyo decides to build a “car audio line”, it will take a long time to get traction, safety approval, planning into new cars.. Will they have the patience/vision to wait and keep pushing the requirements of CE market? Masimo is holding on because it was a billion investment. I’d be curious what a 2.2 billion giant thinks of this 200M investment.. a one time R&D expense?

Thanks Audio G for your kind words and your interesting perspective. It was kind of a challenging story to write, between reading the 8-K and 10-Q (a lot of content) and then dealing with the crux of this issue with its three different forms of intangible assets.

Yes, audio is going through a strange moment. Not helping, is big companies who think they can acquire an audio company because they are easy to fix – not realizing they know nothing about the audio biz.

I’ve studied corporate strategy and learned that 7 or 8 out of every 10 acquisitions fail. Why? Because the acquirer falls in love with the idea of doing a deal and fails to do intensive, objective due diligence. If big companies fought that urge and conducted serious due diligence, they’d realize they have no clue about the audio business and therefore should stay away.

Thanks for reading!

Ted