Both the Index of Consumer Sentiment and the Consumer Confidence Index Drop

The University of Michigan (U of M) has posted its final May report on consumer sentiment, known as the Index of Consumer Sentiment, which follows an earlier preliminary May assessment and finalizes the results. And as I noted in the April report last month, the results remain noteworthy, with a new low reading that exceeds the historically low consumer sentiment reading recorded in June 2022.

The cause of these historically significant readings on declining consumer sentiment, or should I say, increasing consumer pessimism, is the usual suspects – increasing inflation…and the continuing war with Iran.

Read more on this latest historically low reading from the Index of Consumer Sentiment for May…

The U of M Index of Consumer Sentiment is a regularly occurring monthly survey that seeks to understand both how consumers view their current financial circumstances in a sub-survey known as Current Economic Conditions, and how they view the near-term future in another sub-survey known as the Index of Consumer Expectations. These are then combined to create the overall Index of Consumer Sentiment (ICS). Widely watched by economists and the Federal Reserve Board, the ICS has been a reliable indicator of changing consumer views over time.

Consumer Sentiment Drops 10% in May

And in the U.S. economy, the consumer is king. Consumer spending is responsible for about 70% of our gross domestic product (GDP). Optimistic consumers freely spend their disposable dollars, while pessimistic consumers typically save any surplus for a rainy day.

In May, the ICS saw its reading drop to 44.8, down 5 points or a statistically significant 10% from the reading of 49.8 in April. May’s reading was also well below last year’s reading of 52.2 in May 2025. That is a 14.2% decline, year-over-year.

The Cause of This Pessimism? Pretty Simple

It was easy for the U of M analysts to determine the cause for this increasing pessimism.

Consumer sentiment fell for the third straight month as supply disruptions in the Strait of Hormuz continue to boost gasoline prices… The cost of living continues to be a first-order concern, with 57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month.

Joanne Hsu, U of M Surveys of Consumers Director

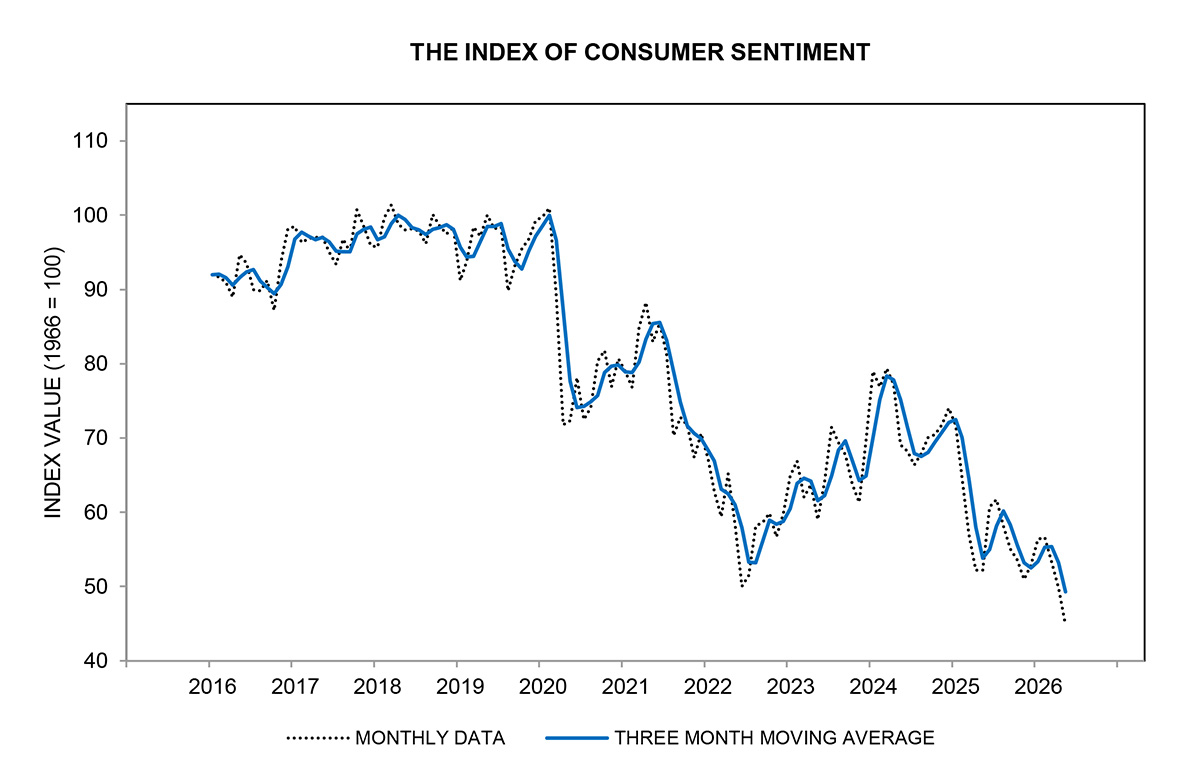

U of M’s Index of Consumer Sentiment continues to set new all-time or historical lows in a trend that started during the COVID-19 pandemic. Here you see month-by-month (blue trace) and a 3-month moving average (dotted trace) [Click to enlarge]

Particularly Strong Sentiment Declines From These Groups

Hsu noted that the survey revealed that lower-income consumers and those without college degrees “posted particularly strong sentiment declines…” as “these groups are more sensitive to increases in the cost of gas and other essentials.”

In a breakdown of results by political affiliation, analysts noted that while the sentiment of Democrats remained similar to last month, “Independents and Republicans saw decreases in sentiment, with both groups reaching their lowest readings of the current presidential administration.”

Critically, consumers appear worried that inflation will increase and proliferate beyond fuel prices, even in the long run.

Joanne Hsu, U of M Surveys of Consumers Director

Consumers Believe Inflation Will Continue to Rise

Survey respondents believe that inflation in the year ahead will reach 4.8%, up slightly over the 4.7% they predicted last month. However, this number is well above what consumers predicted back in February 2026, when they estimated the year-ahead inflation would be at 3.4%. It is currently at 3.8%.

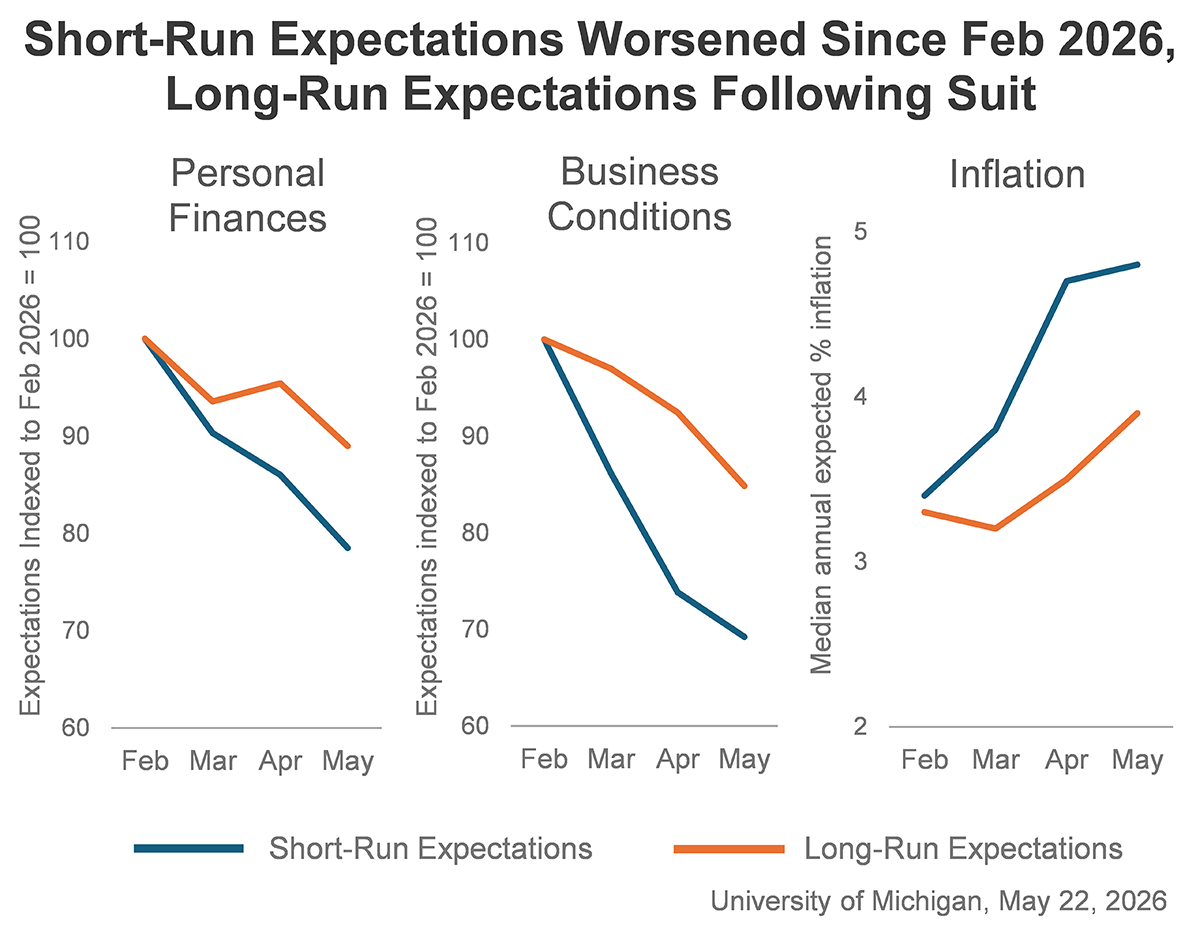

Perhaps to emphasize the importance of the current downward trend, U of M released supplemental charts, like the ones shown here. In each case, the blue trace represents short-run expectations and the gold trace represents long-run expectations. As you can clearly see, consumers view both their personal finances and business conditions as declining dramatically. That feeling extends to their outlook for inflation, which they believe will continue to rise [Click to enlarge]

Similarly, consumers predicted “long-run” inflation would be 3.9%, up from 3.5% in April. The report noted that this 3.9% prediction was notably higher than the 2.8%-to-3.2% prediction range in 2024.

“This month’s increase in long-run expectations reflects sizable jumps among independents and Republicans,” Hsu said. Adding that, especially in the case of Republicans, this new long-run inflation prediction was “double their February 2025 reading…”

The Conference Board’s Consumer Confidence Index Declined More Moderately

Another widely followed consumer survey is the Consumer Confidence Index, conducted by a business group known as The Conference Board. This index is based on a reading of 100=1985, a time of relatively stable prosperity. Readings above 100 suggest improving consumer confidence, which will lead to an expanding economy. Readings under 100 tend to suggest a pessimistic consumer, leading to future economic contraction.

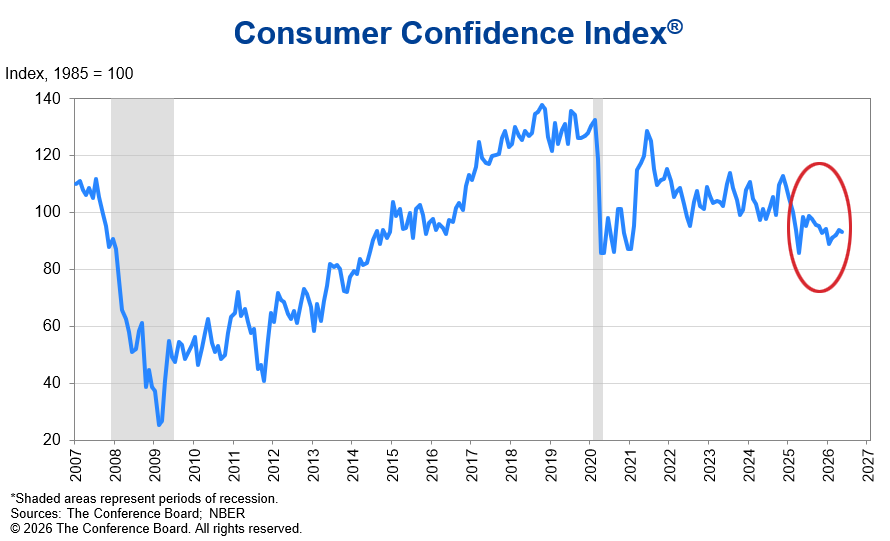

Here you see the Consumer Confidence Index, tracked over a 20-year period. I have highlighted the current 2025/2026 period in a red circle. You can see that confidence began to decline late in 2024 at the end of the previous administration. At the beginning of 2025, there was a burst of confidence at the beginning of the current administration. Since then, however, it has turned negative. There are two things to notice: First, the current level remains below the 100 index line, indicating consumer pessimism; Second, even with a slight bump up here or there, overall the CCI remains at its lowest level since the late 2020 COVID-19 pandemic period [Click to enlarge]

In May, the Consumer Confidence Index (CCI) turned in a reading of 93.1, down from a reading of 93.8 in April. This reading is under the 100 index level, which suggests a pessimistic consumer. But this is not equal to the historic lows recorded by U of M in the ICS.

Current Situation Drops Significantly, Future Prospects Rise Slightly

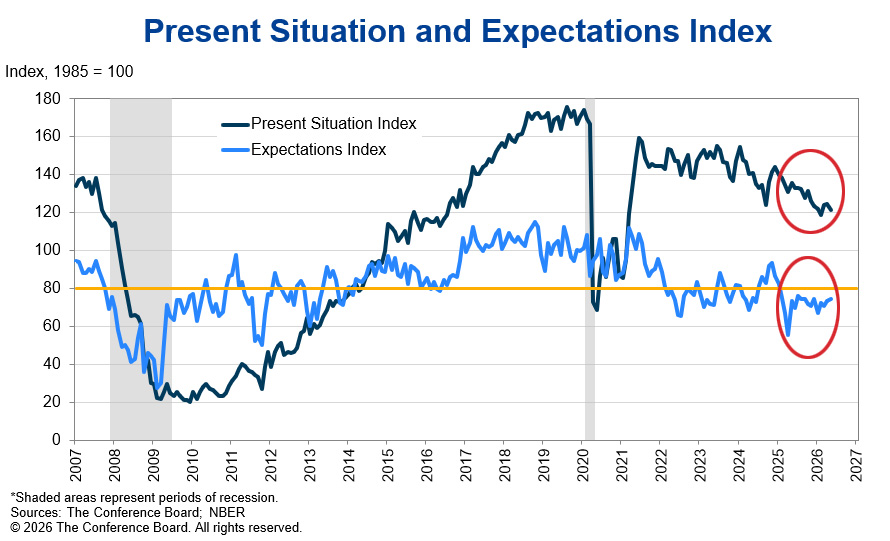

Like the U of M survey, the Conference Board’s CCI also asks consumers about their view of current business and labor market conditions (the Present Situation Index), as well as their outlook for the coming short-term on income, business, and labor market conditions (the Expectations Index). You can see the trend for both of them in the chart below, again with the 2025/2026 period highlighted in a red circle.

In May, the Present Situation Index (dark blue trace) gave a reading of 121.2, down 3.2 points from April. Even though a reading of 121.2 is above the 100 index line, suggesting optimism, the clearly discernible downturn in this reading represents a decided cooling in the feelings of consumers about their present situation.

This chart shows the two main components of the Consumer Confidence Index, the Present Situation Index (dark blue trace) and the Expectations Index (light blue trace). I have highlighted the current 2025/2026 period in a red circle. See more on this chart in the accompanying text [Click to enlarge]

On the other hand, the Expectations Index (light blue trace) – consumers’ view of the near-term future – saw its reading increase by 1.0 point in May to 74.4. That is a slight improvement in consumers’ outlook for the future. But remember, this reading is not only well below the 100 index line, suggesting pessimism, it is also under 80 (note the gold line at 80), which tends to suggest an approaching recession.

The Number of Consumers Anticipating Less Income in the Future is Rising

Consumer confidence edged downward in May as the inflationary impacts of the war in the Middle East intensified. Consumer apraisals of current business conditions and the currrnet labor market were moderately less positive compared to last month. This was somewhat offset by modest improvements in consumers’ expectations for business conditions and the labor market six months from now. Meanwhile, income expectations eased in May, as those anticipating less income rose.

Dana M. Peterson, The Conference Board Chief Economist

So tighten your seatbelts…it’s going to be a bumpy ride.

Leave a Reply