Emerald Holding, Inc. (NYSE: EEX), parent company to Emerald Expositions and owner of the CEDIA Expo, Commercial Integrator Expo, CEPro, Commercial Integrator, and more, reported its financial results for the third quarter of fiscal 2025, showing growth in both consolidated revenues and “adjusted” earnings. However, the data makes it pretty clear that growth relies heavily on acquiring more shows – a costly way to drive growth.

Learn all about the results for Emerald in Q3 of FY 2025…

Emerald reported third-quarter consolidated revenues of $77.5 million for the 90-day period that ended on September 30, 2025. This was an increase of $4.9 million or 6.7% over revenues of $72.6 million in the same quarter in fiscal 2024. However, as you dig into Emerald’s report, you discover that this consolidated revenue number includes multiple new shows added in 2025 that weren’t in the 2024 numbers…in other words, a bit of an inaccurate or an apples-to-oranges comparison.

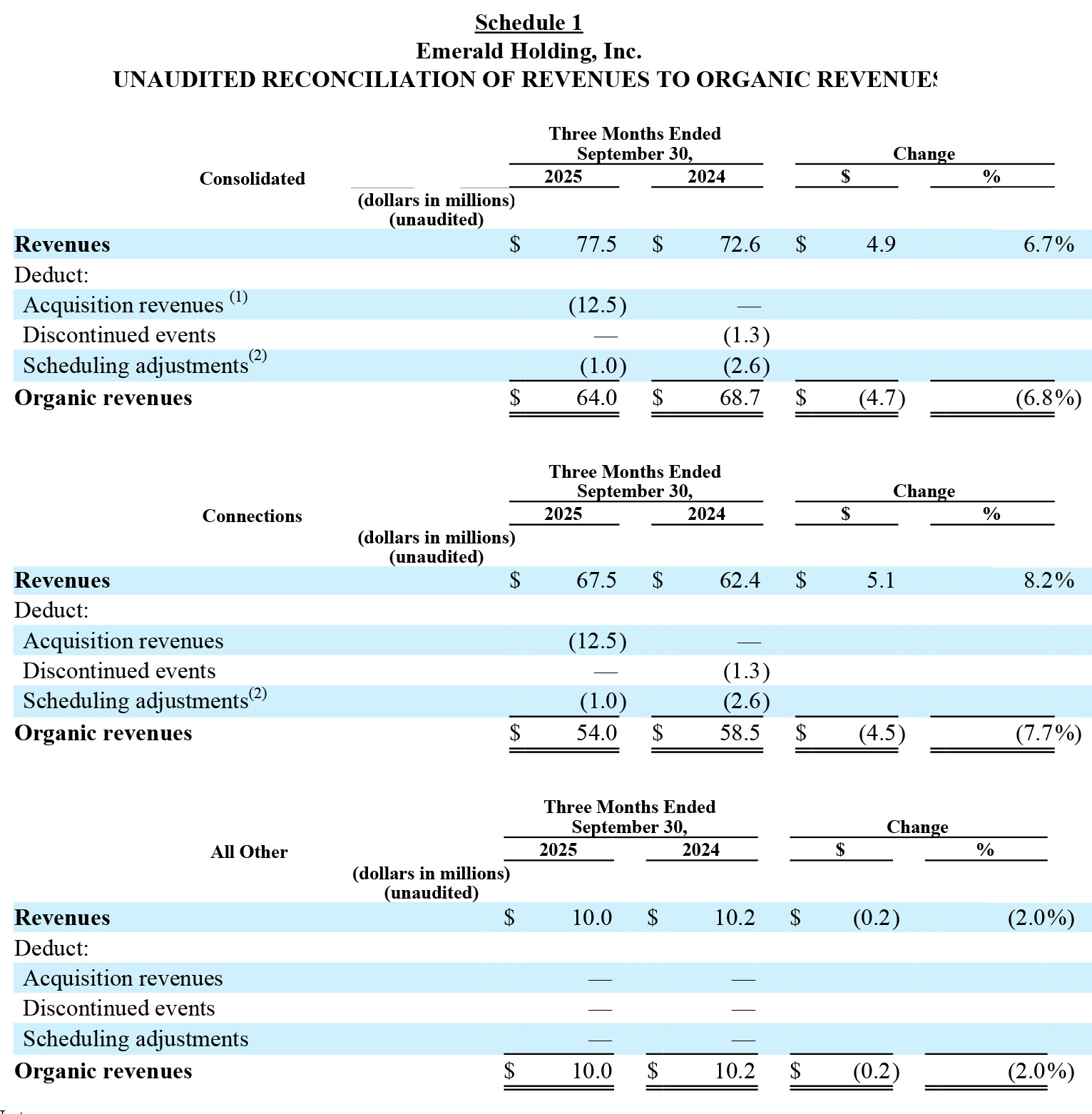

Long-time readers of Strata-gee know I prefer to look at organic numbers – where new shows are removed from the current period’s numbers in order to provide a more accurate read on how the company is performing on an organic, or apples-to-apples basis in ongoing operations. And when we look at Emerald’s organic results, we discover that revenues came in at $64.0 million, a decline of $4.7 million or 6.8% versus the organic revenues of $68.7 million in the same quarter last year.

Relying on a String of Acquisitions to Grow Revenue

What this suggests is that Emerald’s management is relying on a continuous string of acquisitions to drive its ongoing revenue growth. Buying more events is an expensive way to grow your revenues. However, it is part of their two-pronged growth strategy – acquire more shows to add to revenues and drive greater organic growth through leverage and scale. It’s that second part of the plan – drive greater organic growth – that isn’t working so well at the moment. I’ll talk more on that in a bit.

Hervé Sedky

Throughout the year, Emerald has continued to execute with discipline and consistency across the portfolio, advancing the strategic priorities we outlined at the start of 2025. Even in what is traditionally our softest quarter, our teams remained focused in the third quarter and continued to deliver meaningful progress across the business. We strengthened our portfolio through the acquisition of Generis and advanced innovation initiatives, such as early-stage AI tools, designed to enhance the customer experience and deliver scalable efficiency in our processes. These actions reflect our focus on building dynamic, high-impact platforms that help businesses connect and grow in an increasingly complex marketplace. Strong rebooking trends and solid pacing for 2026 underscore the confidence customers place in our platform and the enduring value of live events.

Hervé Sedky, Emerald President and Chief Executive Officer

Breaking Down Emerald’s Business Segments and Tracking Units

A sampling of the shows that Emerald owns. [Click to enlarge]

Emerald addresses three main business segments:

CONNECTIONS – This is by far its largest business segment, and it consists of around 100 (including the number of media products in the content segment below) B2B trade shows, conferences, and other industry events. It is in this segment that CEDIA Expo and Custom Integration Expo reside. Connections represents around 90% of Emerald’s total revenues.

CONTENT – This segment consists of B2B websites and publications across 20 industry sectors. It is in this segment that CEPro and Commercial Integrator reside. Content represents only about 5% of total revenues.

COMMERCE – This business segment consists of wholesale e-commerce software and marketplace service offerings. Emerald actually acquired the company that makes the software technology that runs the B2B e-commerce site. Originally, management had big plans and expectations for scaling this unit, but it does not appear to be growing significantly. Like Content, Commerce represents only around 5% of total revenues.

Because CONTENT and COMMERCE do not meet the qualifications to be tracked as an independent business unit, the company lumps them together in a single unit called “All Others.” So they track their business in two units: Connections…and…All Others.

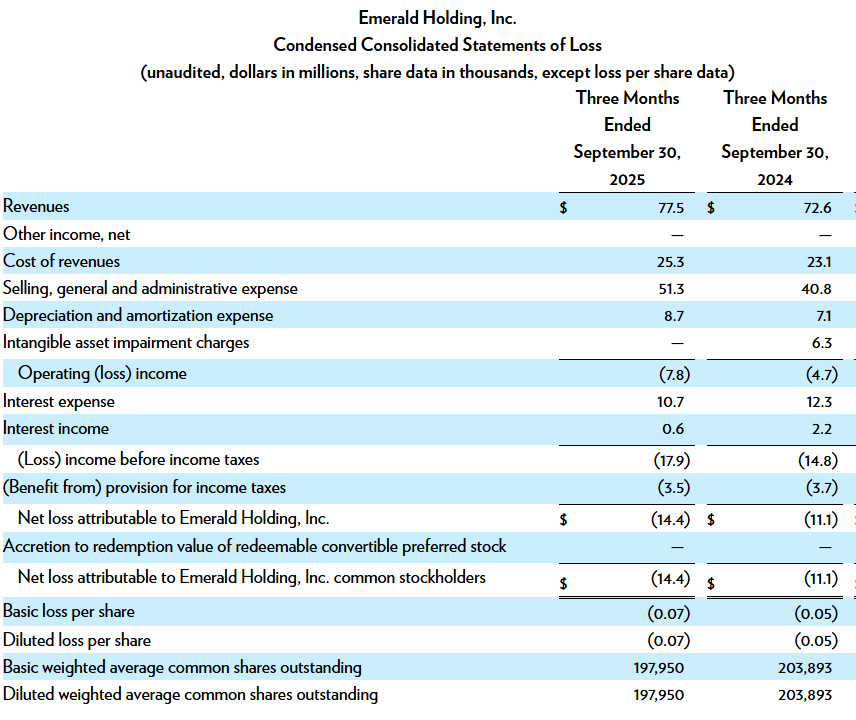

This table presents the Condensed Consolidated Statements of Loss. Revenues grew by $4.9 or 6.7% to $77.5 million. The company had an Operating loss of $7.8 million and a Net loss of $14.4 million [Click to enlarge]

Three New Acquisitions in 2025

Emerald acquired three new events in 2025: Insurtech Insights (events centered around insurance technology, acquired March 2025), This is Beyond (London-based company with 7 shows on luxury travel event business, acquired May 2025), and Generis (Canadian-based promoter of executive summits in manufacturing, pharma, and industrial spaces, acquired August 2025). The company does not reveal revenues from individual events, but from its commentary, it appears as though Generis is the largest of the bunch.

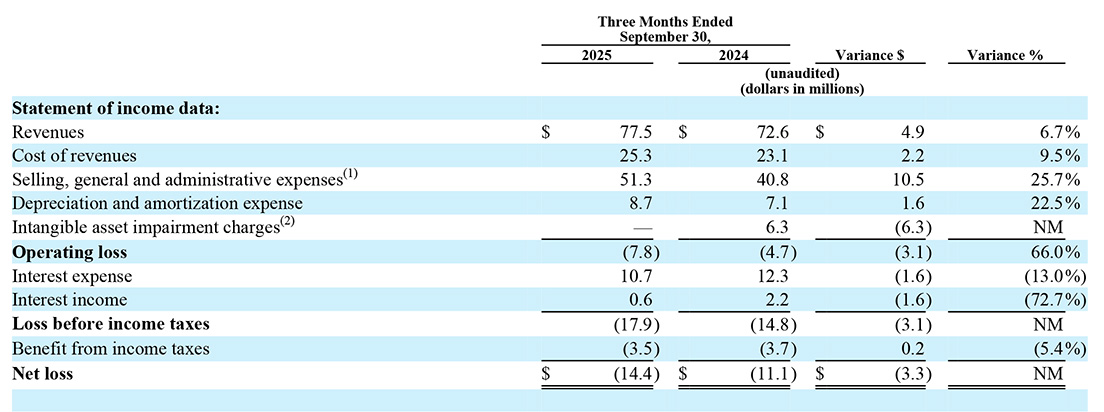

Returning to the company’s quarterly performance, as I mentioned above, the company’s consolidated revenues grew, and the company seems pleased with that. However, various costs and expenses also grew, many even more than revenues. That can be a problem… For example, consolidated revenues (including new events added this year) grew by 6.7%, but at the same time Cost of revenues grew by 9.5%…Selling, general, and administrative expenses (SG&A) grew by a surprising 25.7%, and Depreciation and amortization expense grew by 22.5%. Click on the table below to see a larger version with the percentage of growth included.

This view of results adds in both dollar and percentage variance. You can see here how expenses grew at a greater pace than revenues [Click to enlarge]

Revenues Increased…Expenses Increased More

The company explained the surprising jump in SG&A expense as largely connected to acquisition-related charges, as well as “legal, audit and advisory fees” (probably also connected with the acquisitions). Whatever the reason for the elevated charges, the bottom line is that even in the face of a growth in revenues, the company generated an increased Operating loss this year of $7.8 million, $3.1 million or 66.0% higher than the operating loss of $4.7 million in the same quarter last year.

Next, we find that Emerald’s Net losses also increased in Q3. The company reported it generated a net loss of $14.4 million, $3.3 million or 30% greater than the $11.1 million net loss in the same quarter last year.

Disaggregating Revenues Offers More Detail

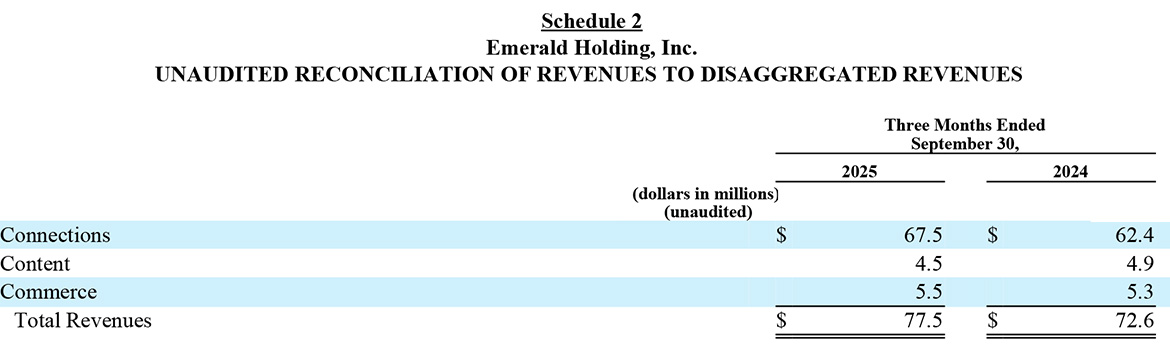

The table below provides a disaggregation of the consolidated overall revenues by each of the company’s business segments. These numbers include the new events added this year. As you can see, both Connections and Commerce showed revenue increases, although the Commerce increase is slight. Only Content, the business unit with CEPro/Commercial Integrator media properties included, showed a decline to $4.5 million in revenues in the quarter this year. This result is down $0.4 million or 8.2% compared to revenues of $4.9 million in Q3 of fiscal 2024.

This table shows a breakdown of the business segments that Emerald addresses. These numbers include new events added this year [Click to enlarge]

Reorganizations of Content and Commerce Don’t Appear to Bear Fruit

In previous reports, I told you how that company had implemented two major reorganizations of the content unit in an effort to reinvigorate its performance. Recently, I reported more changes at CEPro as Bob Archer’s position was eliminated from the company. This followed Arlen Schweiger’s departure some time back and Jason Knott’s exit before that.

Clearly, the reorganizations implemented by Emerald management have not succeeded in revitalizing the media group. Emerald CEO Hervé Sedky told analysts on a recent earnings conference call that Emerald’s many media properties were largely being transformed into a lead generation vehicle serving the shows to which they are attached (CEDIA Expo in our case). He gave no details on just what this means in terms of their editorial strategy, if any.

Both Content and Commerce are Under-Performers at Emerald

On top of this, the company had made a significant investment in its Commerce business, where it envisioned dramatically scaling it to substantial, year-round revenue. Like Content, the company had restructured the Commerce business as well, which is operating. But as you can see from the numbers, it is not a big contributor to the company’s financials.

Company executives really didn’t talk about either of these divisions during their prepared presentations. Only when they opened the earnings call up for questions did they address it. When asked directly about both Content and Commerce, Sedky said this…

Content and Commerce are in an Evolution Phase

“I think both on content and commerce…[he paused]…it’s an evolution of both businesses,” Sedky explained. “On the content side, as you know, it’s been an area that has been an anchor to our growth. We have been investing in continuously shifting that business from relying on advertising to being more of a lead-gen model. We’re making some very good progress, especially in the last few months, which I’m very, very happy about. We’ll report about that in the coming quarters.

“On the commerce side, we’ve really shifted our focus to one of profitability,” Sedky added. “We’ve made some material progress in terms of really driving a profitable commerce business, whereas it went from unprofitable to break-even to now a contributor to EBITDA, which we’re very, very happy with the team’s progress on that front.”

By the way, when Sedky says Content is an “anchor” to Emerald’s growth, he means it is slowing down and hurting the company’s business. And when he says that on Commerce, they are focusing on profit, it suggests he’s shifting focus away from scaling up that business…perhaps cutting investment into it as well.

Details on the Organic Numbers

The three tables shown above reveal the true “organic” results for Emerald in the quarter. The top table is the total combined result (“Consolidated”) that sums the two independent business units (“Connections” and “All Other”). Remember, All Other includes both the Content and the Commerce segments combined.

Organic Revenues Decline

This data shows you that Connections had total organic revenues of $54 million in the quarter, down $4.5 million or 7.7% compared to the organic revenues of $58.5 million in the same quarter last year. The other business unit – All Other – had total organic revenues of $10.0 million in the quarter this year. This is down $0.2 million or 2.0% compared to organic revenues of $10.2 million in Q3 in fiscal 2024.

The company says that the third quarter is historically its smallest and softest period. Even so, they claim this year, the quarter came out “largely as expected.” Clearly, the numbers bear this out and the company maintains it expects the year to finish as they originally projected.

More Work to be Done

Still, there appear to be some dark clouds with Content and Commerce units underperforming the Connections division. Not to mention that profits are being stunted by the added investments required when acquiring more events. Even with 100 events in its portfolio, Emerald doesn’t appear to be fully leveraging those businesses to begin driving greater profit growth.

Learn more about Emerald by visiting emeraldx.com.

Leave a Reply